By Jim Shimabukuro (assisted by Claude)

Editor

Summary: The global data‑center surge exposes a paradox: the infrastructure powering AI’s future is becoming one of the world’s most misunderstood and politically contested industries. –Copilot

Something is off in the way data centers are discussed publicly versus how they are understood within the technology industry. Outside observers hear about enormous power consumption, dried-up aquifers, tax breaks handed to some of the world’s richest corporations, and warehouses full of servers that create almost no permanent jobs. Inside the industry, the same buildings look like the physical backbone of a technology transition that will define the next decade — and investors who once worried about a bubble now watch capacity lease up as fast as it can be built.

Both pictures are accurate. The disconnect is not dishonesty on either side; it is that each side is describing a real but partial view of the same phenomenon. This report tries to bring those views together, covering what is actually driving construction, what is driving resistance, where nuclear power fits in, what is really going on with Starlink, and why data centers have become inseparable from questions of national security and AI supremacy.

The numbers attached to data center construction are genuinely large by any historical standard. More than 35 gigawatts of capacity is currently under construction in North America — a figure that would have been unimaginable five years ago (1). US spending on data centers was forecast to top $425 billion in 2025 (2). The four hyperscalers — Alphabet, Amazon, Microsoft, and Meta — announced plans to invest more than $350 billion in data centers in 2025 alone, with approximately $400 billion planned for 2026 (3). Data center construction spending grew nearly 30 percent year-over-year in late 2025 (30).

Industry analysts tracking occupancy rates see little sign of the bubble that some observers have predicted. Vacancy across major markets sits close to one percent, and 92 percent of the capacity currently under construction is already committed under binding lease agreements or owner-occupied development (1). The companies signing those leases rank among the most creditworthy borrowers in the global economy.

The forecasts for further growth are equally striking. S&P Global estimates that US data center grid-power demand will rise 22 percent in 2025 to 61.8 gigawatts, climb to 75.8 gigawatts in 2026, and reach 134.4 gigawatts by 2030 (9). The sector is projected to add approximately 97 gigawatts of capacity between 2025 and 2030, which would nearly double its total size within five years. More than 4,000 data centers are already operating in the United States, with 3,000 more planned or under construction (2).

Against that backdrop of investment and growth, public sentiment has turned sharply negative — and for reasons that hold up under scrutiny. A 2026 Pew Research Center poll found broad public concern about the impact data centers have on electricity rates, water supplies, and local environments (6). Between January and March 2026 alone, opposition groups blocked or delayed at least 75 data center projects nationwide, representing nearly $130 billion in stalled investment, and the number of active opposition groups more than doubled to 833 across 49 states (4).

Ben Green, a faculty associate at Harvard’s Berkman Klein Center for Internet and Society, told the Harvard Gazette in April 2026: “I think the public is quite right to be concerned about data centers. It’s a sort of David and Goliath fight; local communities are pushing back against some of the wealthiest companies in the world.” (6)

The electricity concerns are substantive. Within a few years, data centers could account for 10 to 15 percent of total nationwide electricity demand (6). In some PJM Interconnection service territories — covering much of the Mid-Atlantic and Midwest — capacity cost increases driven by data center load growth have pushed retail electricity prices up by more than 15 percent (10). Residents near data centers find their electric bills rising to subsidize infrastructure built for trillion-dollar corporations.

Water use adds another layer of public concern. Texas data centers alone are estimated to consume 49 billion gallons of water in 2025, with projections reaching 399 billion gallons by 2030 — enough to draw down Lake Mead by more than 16 feet in a year. Five hundred seventeen of the 809 data centers planned in the United States are located in areas that experienced drought in the past year (7). A Google facility in South Carolina faced sustained opposition over its proposed groundwater use; an xAI data center in Memphis alarmed residents with its proposed daily withdrawals from aging public infrastructure (4). In California, data center construction expanded throughout 2025 and into 2026, yet lax disclosure rules kept water usage figures from the public (8).

The jobs argument that developers use to win state tax breaks has proven largely hollow. Green’s research found that once construction ends — typically after one to two years — a data center employs just 20 to 50 people, because a warehouse of servers does not require marketing teams or software engineers. Over the past year, Virginia and Georgia together gave up more than a billion dollars in tax revenue through data center incentives, with little evidence of commensurate local benefit (6). In 2026, lawmakers in more than 30 states introduced over 300 bills addressing data center development, including moratoriums, tax policy changes, and energy requirements. More than 230 environmental organizations issued a collective call to Congress for a national moratorium on new data center construction (8).

The most concrete constraint on data center growth is neither public opposition nor capital costs — it is electricity. The grid was not designed for what is now being asked of it.

PJM Interconnection’s analysis reveals a potential 49-gigawatt US generation shortfall by 2028, the result of surging data center demand colliding with planned retirement of aging coal and gas plants and slow interconnection timelines (10). In some cases, requests for grid connection face a seven-year wait in the queue (5). Building regional transmission lines currently takes seven to eleven years just for permitting. Large power transformers now average 128 weeks of lead time; generator step-up units average 144 weeks — meaning the supply chain for the physical equipment needed to expand the grid is nearly as constrained as the grid itself (10).

The Information Technology and Innovation Foundation concluded in November 2025 that data center energy demand, while real and growing, is not inherently a problem if the right policy responses follow — primarily transmission permitting reform and a faster interconnection queue (11). Deloitte’s analysis reached a similar conclusion: the challenge is a structural mismatch between the pace of demand growth and the pace at which regulatory and physical infrastructure for new power generation can be assembled (5).

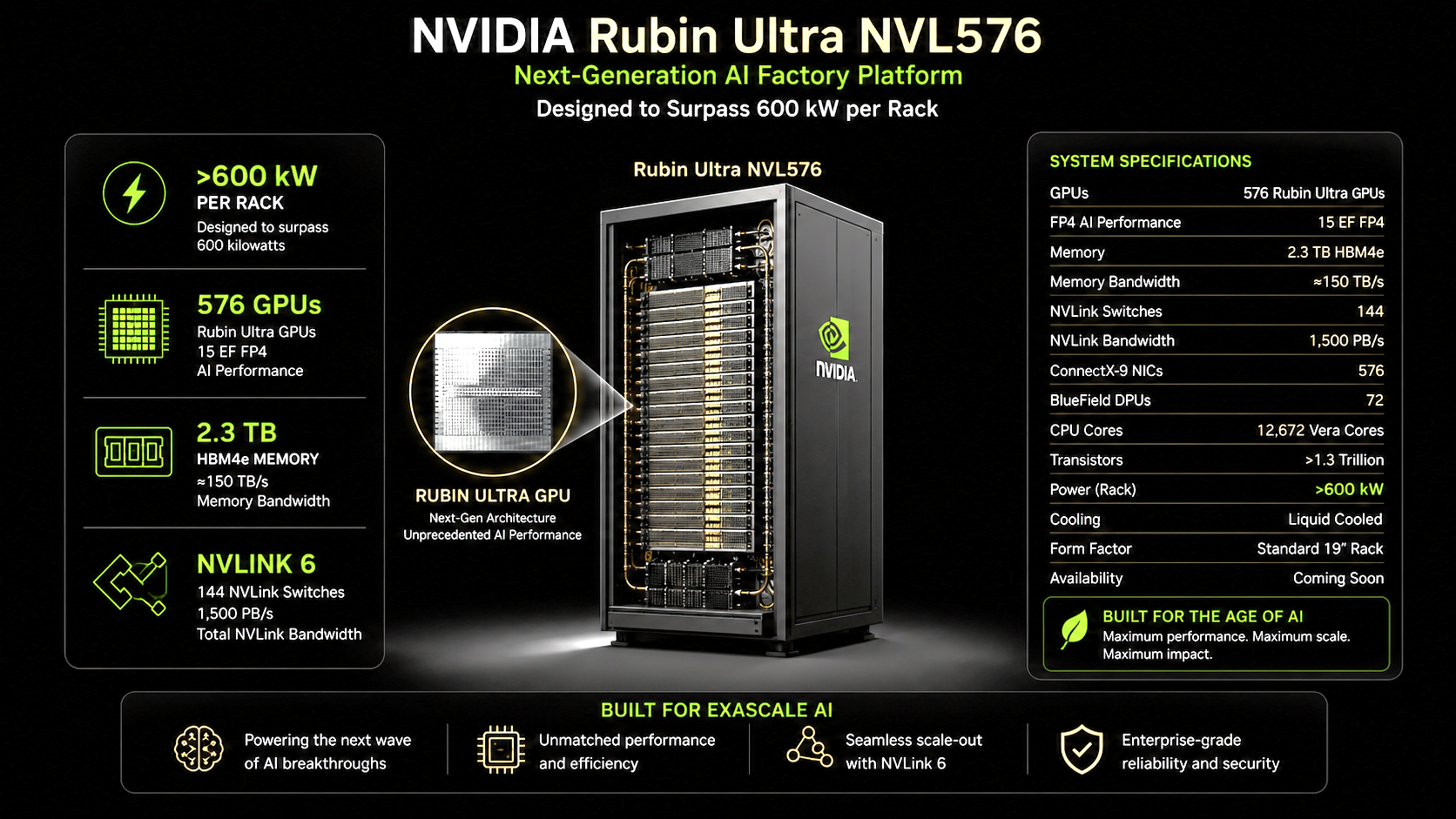

The scale of power demands per rack has escalated sharply in recent years. Nvidia’s Blackwell GB300 rack systems required 163 kilowatts per rack in 2025; the Vera Rubin NVL144 systems arriving in 2026 are projected to exceed 300 kilowatts per rack; and the Rubin Ultra NVL576 is expected to surpass 600 kilowatts per rack (27). That escalation strains not just the external grid but the cooling and electrical infrastructure inside data centers themselves.

The energy bind created an opening for nuclear power that the industry has moved quickly to fill. Data centers need electricity that is consistent, dispatchable, and available around the clock — properties that wind and solar cannot guarantee without large-scale storage. Nuclear, whether from existing plants or from new designs, fits those requirements precisely.

In 2025, Microsoft and Constellation Energy reached a 20-year agreement to restart Three Mile Island Unit 1 — the Pennsylvania reactor shut down for economic reasons in 2019 — to provide power for Microsoft’s data centers (12,13). AWS and Talen Energy signed a 17-year power purchase agreement for 1.92 gigawatts from the Susquehanna nuclear plant in Pennsylvania. Meta struck 20-year agreements to purchase electricity from three nuclear plants, while also joining Oklo and TerraPower in a small modular reactor development project (12). Google and Kairos Power announced plans to deploy an advanced nuclear facility tied to the Tennessee Valley Authority grid (13).

The small modular reactor, or SMR, has attracted particular attention because its scale aligns well with data center needs. Traditional nuclear plants produce 1,000 megawatts or more — far more than a single data center requires and far more expensive to build. SMRs are designed to produce between 50 and 300 megawatts, can be built in factories and assembled on site, and can be located closer to load centers (14,17). The Department of Energy has noted that data centers create near-ideal conditions for SMR deployment: enormous, concentrated demand that must be met continuously, with operators willing to sign the long-term contracts that make nuclear financing feasible (16).

The path is not without difficulty. SMR designs in the United States remain largely in the licensing and early construction stage, meaning the technology’s near-term role is primarily through agreements with existing plants rather than new builds. The Nuclear Regulatory Commission’s approval processes, designed for large light-water reactors, are being adapted for new reactor types, but the adaptation is slow (15). Still, the direction is clear: nuclear is being repositioned from a declining legacy industry to a preferred baseload partner for the most capital-intensive infrastructure build in recent memory.

Starlink tends to appear in gloomy narratives because early coverage focused on growing pains that were real but predictable. The more recent picture is substantially different.

SpaceX’s 2025 Progress Report showed that average US download speeds grew from roughly 23 megabits per second in 2022 to over 170 megabits per second by late 2025, while latency improved from 44 milliseconds to approximately 24 milliseconds over the same period (18). The constellation expanded to more than 9,400 satellites following more than 100 launch missions during 2025 alone (18,20). The service now has over 6 million customers globally, having added 2.7 million over the past year — an annual growth rate of 82 percent (19).

The problems are real but attributable to growth rather than to fundamental design failure. In areas with high subscriber density, network congestion during peak evening hours can reduce speeds from around 150 megabits per second to 50–80 megabits per second (21). SpaceX introduced a congestion surcharge of $100 in saturated markets, raising it to $250 in some cities — a blunt commercial response to a genuine capacity problem (21). Users in lightly populated rural areas, by contrast, consistently report performance in excess of 200 megabits per second, which is the use case the system was originally designed to serve (19).

The remedies are already underway. The FCC approved a 50 percent increase in the total number of Starlink satellites SpaceX can deploy, raising the ceiling from roughly 12,000 to 19,000. Third-generation satellites, planned for 2026, are larger and carry significantly more capacity than those currently in orbit (21). The FCC also approved increased operating power for dishes, which improves performance in marginal coverage areas and has allowed SpaceX to eliminate congestion fees in several previously affected markets (20). These are the hallmarks of a service experiencing the friction of rapid scaling, not the signs of a structurally broken architecture.

The geopolitical stakes attached to data centers have risen sharply and now touch questions of national security. The United States hosts roughly 51 percent of the world’s data centers; China is second at about 22 percent (22). That asymmetry is not lost on any party in the current technology rivalry.

In his July 2025 “America’s AI Action Plan,” President Trump stated: “It is a national security imperative for the United States to achieve and maintain unquestioned and unchallenged global technological dominance” (24). The Modern War Institute at West Point addressed the question in concrete terms, arguing that data centers represent “key terrain” in future conflicts — infrastructure that must be defended and, if necessary, denied to adversaries (25).

The race has produced responses from other regions. At the February 2025 AI Action Summit in Paris, EU Commission President Ursula von der Leyen announced InvestAI, a €200 billion initiative for AI infrastructure investment across Europe. China is expected to press its open-source AI strategy through 2026 as a way of shaping the global AI infrastructure stack in its favor (23). The pattern — concentrations of compute capacity translating into concentrations of geopolitical influence — has prompted governments to mandate that sensitive data be processed on home soil, fragmenting what was once a borderless cloud into national silos (22).

The connection between data centers and AI capability is direct: training a large AI model requires weeks or months of continuous computation across thousands of accelerators, and inference — the process of running a trained model — requires sustained throughput at scale. A country without the physical infrastructure to perform that computation at a competitive level depends on entities that do have it, accepting both the latency and the surveillance risk that dependency implies. As the World Economic Forum observed in mid-2025, international relations are now defined as much by control of data infrastructure as by traditional geopolitics (23).

The shift to agentic AI — systems that act autonomously on multi-step tasks rather than simply responding to single prompts — is changing not just how much compute data centers need but what kind of compute they need.

Traditional AI deployments, such as chatbots and content generators, are predominantly GPU-bound: they run one inference pass per user query and return a result. Agentic systems are architecturally different. They plan, break tasks into subtasks, call external tools, maintain context across long sessions, spawn subagents to handle parallel work streams, and loop through reasoning cycles without waiting for a human prompt at each step. Analysts at Quartz reported that AI agents can consume 1,000 times more tokens than a single chatbot query, before accounting for the coordination overhead of multi-agent pipelines (26).

That shift is creating a bottleneck that neither the industry nor outside observers fully anticipated: the CPU. Where GPU-heavy workloads dominate model training and single-pass inference, agentic workloads land heavily on the CPUs responsible for orchestrating agents, managing memory, and directing tool calls (26,27). The industry response has been a wave of CPU designs built for AI coordination. Nvidia’s Vera CPU, announced at CES 2026 and entering deployment in the second half of 2026, features 88 custom Arm-based cores and delivers up to 1.2 terabytes per second of memory bandwidth (27). Arm’s AGI CPU, introduced in March 2026, carries 136 Neoverse V3 cores and is purpose-built for the orchestration workloads that agentic systems generate (29). Analysts project that agentic AI will require data centers to deliver up to four times the CPU core density within the same power envelope as today’s facilities (27).

The infrastructure implications extend beyond chip selection. Data centers built for training workloads optimized for sustained, predictable GPU utilization. Agentic workloads are bursty, with demand patterns driven by autonomous agents that spin up and down unpredictably, call external services on variable timelines, and maintain context over hours or days rather than milliseconds. The architectural difference is significant enough that many analysts expect purpose-built agentic AI data centers to emerge as a distinct facility category, separate from training clusters and inference farms (27,28).

The energy trajectory underlying all of this continues to accelerate. From 80 gigawatts of US data center energy demand in 2025, projections point to 150 gigawatts by 2028 (10). The industries supplying data centers — chipmakers, cooling system manufacturers, fiber providers, power equipment companies — are running at or near capacity, with lead times measured in years rather than months.

The perception gap surrounding data centers is real, but the two sides of the debate are not simply talking past each other — they are observing different aspects of the same transition. Communities near proposed data centers see the costs: rising electricity bills, strained water supplies, tax concessions that benefit shareholders rather than local residents, and construction-phase jobs that disappear once the building is done. Technology investors and policymakers see the demand: an AI build-out with no near-term ceiling and a geopolitical context in which falling behind is not a commercially neutral outcome.

Starlink is experiencing the friction of rapid growth, not structural failure. Nuclear power is being repositioned from a declining legacy industry to a preferred baseload partner for the most capital-intensive infrastructure build in recent memory. The shift to agentic AI is changing not just the scale but the character of what data centers must do — pushing hardware designers, architects, and operators into territory that none of them fully anticipated even three years ago.

The gloomy reports and the investment optimism are both accurate as far as they go. What they share, and what most coverage misses, is the scale of the bet being placed. The physical infrastructure going into the ground now will determine, to a substantial degree, who shapes the next generation of AI and on whose terms it operates.

References

1. JLL, “North America Data Center Report Year-end 2025”

2. Programs.com, “Measuring the Data Center Boom: Facts and Statistics (2026)”

3. JLL, “2026 Global Data Center Market Outlook”

5. Deloitte, “Can US infrastructure keep up with the AI economy?”

6. Harvard Gazette, “Why are communities pushing back against data centers?”

7. Lincoln Institute of Land Policy, “Data Drain: The Land and Water Impacts of the AI Boom”

8. CalMatters, “Data centers are guzzling California’s water. We have no idea how much.”

9. S&P Global, “Data center grid-power demand to rise 22% in 2025, nearly triple by 2030”

10. Data Center Knowledge, “Gridlocked: How Power Constraints Are Shaping the Future of Data Centers”

12. Morgan Lewis / Data Center Bytes, “2026 US Data Centers and Energy: Key Trends Shaping Power Demand”

13. Deloitte, “Nuclear energy’s role in powering data center growth”

15. Reason, “Next-generation nuclear power can meet data center energy demand—if regulations allow it”

16. U.S. Department of Energy, “Advantages and Challenges of Nuclear-Powered Data Centers”

17. iRecruit, “SMR Data Centers: How Small Modular Reactors Power AI Infrastructure (2026)”

18. SpaceX / Starlink, “Starlink Progress Report 2025”

19. US Mobile, “Starlink Internet Review 2026: Speed, Reliability & Real-World Performance”

20. CircleID, “Starlink Update: Expansion, Performance Gains and Network Developments”

21. SatelliteInternet.com, “Starlink Roadmap 2026: More Changes For More Speed and Capacity”

22. S&P Global, “Geopolitics of data centers: An AI showdown that will reshape the world”

23. World Economic Forum, “AI geopolitics and data in the era of technological rivalry”

24. The Washington Post (Opinion), “Data centers are critical to AI, military and national security”

26. Quartz, “Why agentic AI compute demands are reshaping data centers”

27. Semiconductor Engineering, “Agentic AI Is Changing Data Center Architectures”

28. AMD, “Agentic AI Brings New Attention to CPUs in the AI Data Center”

30. ABC Carolinas, “Data Center Construction Spending: Trends and Economic Impact Analysis”

###

Filed under: Uncategorized |

{kind=link}

What are the main environmental, economic, and social concerns surrounding the rapid expansion of data centers, and why are they becoming controversial among local communities? LINK